BILT 2.O CARDS – THE REAL SCOOP

New Cards Sparkle, but Offer has Lost Some Lustre and Complexity Abounds

ANALYSIS

Max Plastic

1/21/202611 min read

Introduction:

The Bilt 2.0 offer is here, and my how things have changed! The offer has expanded from one card to three, ranging from a no fee card with minimal benefits to a $495 fee card with multiple credits and benefits.

First and foremost, Bilt has kept their promise and expanded their rent rewards program to include mortgages (to keep language simple, wherever I refer to ‘rent’ in this article, feel free to insert ‘mortgage’; they are interchangeable). They continue to waive transaction fees on rent payments, have removed the 100,000 annual rent point earning limit, and have made it clear that the same card can be used to pay multiple rents. All of this being said, there are new spending criteria that must be met to “unlock” points associated with rent. These criteria are exceptionally complex, and I have done more math to fully understand them in the past few days than I did in college!

The prior version of the Bilt card was a no-brainer for anyone who paid rent. Is the 2.0 version still worth it? It depends on how much you’re willing to use the card for non-rent purchases, which is what they’re trying to drive. In this article I’ll break down the mechanics and options so you can make an informed decision.

This article includes:

What is Bilt?

Bilt Credit Cards

Paying Rent with Your Bilt Card:

Non-rent to Rent Ratio

Bilt Cash

Card Offering

Card Comparison Table

Max’s Takes

What is Bilt?

Before I explain the ins and outs of the Bilt credit cards, I should first describe what is Bilt, because this can be quite confusing even before trying to describe their new credit card offer. If you’re already familiar with this, skip ahead to the next section.

Forget about credit cards for the moment. Bilt is a platform that enables you to pay rent without transaction fees and earn points for certain purchases. They have a neighborhood focus, marketing themselves as a “membership for where you live”. They focus on bringing you enhanced and exclusive benefits where you live, through neighborhood partners like your mortgage provider, landlord, local restaurants, fitness studios, Lyft, Walgreens and more. To realize these benefits, you must first sign up in the portal. This makes you a member of the Bilt Rewards Program, and it is free of charge. You then link a credit card(s), a bank account(s), or both to your Bilt “wallet”. In exchange for this, Bilt has full visibility to each linked account.

The points earned in the program can be used as credits to your account, to offset rent payments, or transferred to Bilt travel partners for redemptions.

In line with their neighborhood focus, the Bilt Rewards Program offers multipliers for purchases with “neighborhood” partners. They are:

3x points on Lyft Rides

3x points at partner fitness studios

3x points at partner restaurants

2x points at Walgreens

2x points on hotels booked through the Bilt portal

1x points on airfare booked through the Bilt portal

So, let’s say you link a credit card, that earns 1 point for every dollar spent, to your Bilt wallet and used that card for $20 a Lyft ride. You would earn 20 points on your credit card account, AND you would earn 60 points in your Bilt account.

The rewards membership program can also be linked to your Rakuten account, enabling you to earn additional points through that program as well.

Are you still with me?

Bilt Credit Cards

Now, back to Bilt credit cards. Bilt supplements their membership offer with their own credit card. You do not need a Bilt credit card to become a Bilt Rewards Member. In fact, Bilt claims that only about 15% of Bilt Rewards Members have a Bilt credit card.

Acquiring a Bilt card automatically enrolls you as a Bilt Rewards Member, providing you access to neighborhood partner programs. It also enables you to earn points on rent payments. You must have a Bilt card to earn points on rent payments. It also provides points and point multipliers for everyday purchases, which are stacked on top of those offered in the Bilt Rewards Program, just as linking an external card would.

As mentioned in the introduction, Bilt has expanded their credit card offer from one card to three. No matter which of the three cards you have, the options and rewards specifically for paying rent are the same. Since rent payment is the focus of the Bilt cards, I’ll address rent payments first, then I’ll address the card offering.

Paying Rent With Your Bilt Card:

Until this change, Bilt offered 1 point for each dollar of rent paid, as long as the Bilt card was used at least 4 additional times in the payment cycle for non-rent purchases. This approach took a serious bite out of Bilt’s profitability, as cardholders soon found that they could use their card for four small purchases, on which transaction fees were paid, and one large rent, on which no transaction fees were paid. Bilt’s current offer is designed to encourage more significant use of the cards for everyday purchases to drive up transaction fees.

There are now two options to earn points through paying rent, both of which operate under the same premise. The more you use your card for non-rent purchases, the greater the rewards you will earn through rent. The math can get a bit complex, so I’ll start with the simpler option first.

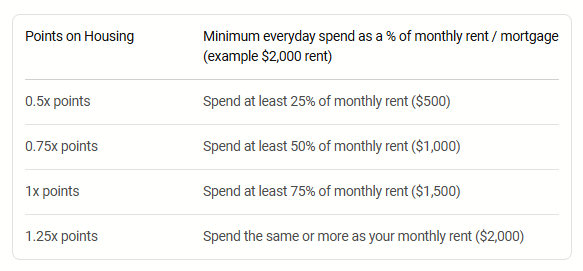

Option 1: Points Chart

Bilt will award points increasingly for rent spend depending on how your non-rent spend on the card compares to your rent spend. The table below reflects how the rent reward increases as the ratio increases, using an example of $2,000 rent:

As an example, if your non-rent spend in a period is equal to or greater than your rent spend, Bilt will award 1.25 points for each dollar of rent spend you have. In this case, for a $2,000 rent spend, you will earn 2,500 points. Conversely, if your non-rent spend is between 25% and 50% of your rent spend, Bilt will only reward ½ points for each dollar of rent spend you have. In this case, for the same rent spend of $2,000, you’ll only earn 1,000 points.

Option 2: Bilt Cash

Confused yet?...keep reading. The second option is more complex.

As you use your Bilt card for non-rent purchases, you earn 4% back in Bilt Cash. That Bilt Cash can then be applied to your rent to “unlock” points. The points you unlock are yours to keep. Points are unlocked at a rate of 100 points per $3 in Bilt Cash. You determine how much of your available Bilt Cash to use each month. At the end of the year, only $100 of Bilt Cash can be carried into the new year, so you want to be sure to use what you have.

Let’s take an example, using the same $2,000 per month rent, and $500 in non-rent purchases. The $500 spend would earn you $20 ($500 x 4%) in Bilt Cash.

That Bilt Cash can then be converted to unlocking 667 points ($20 x 100/$3).

To unlock the full 2,000 rent points, we can do the math in reverse:

2,000 x $3/100 = $60 Bilt Cash. $60 / 4% = $1,500.

So to unlock the full amount of 2,000 rent points possible, you would need to use your card for $1,500 of non-rent purchases in the same period. This is a ratio of 75% ($1,500 / $2,000). This ratio of 75% applies to any amount of rent. For example, to unlock all possible points for a $4,000 rent, the card needs to be used for $3,000 in non-rent purchases that same period.

Check out Max's Takes below to our analysis on which is the better option.

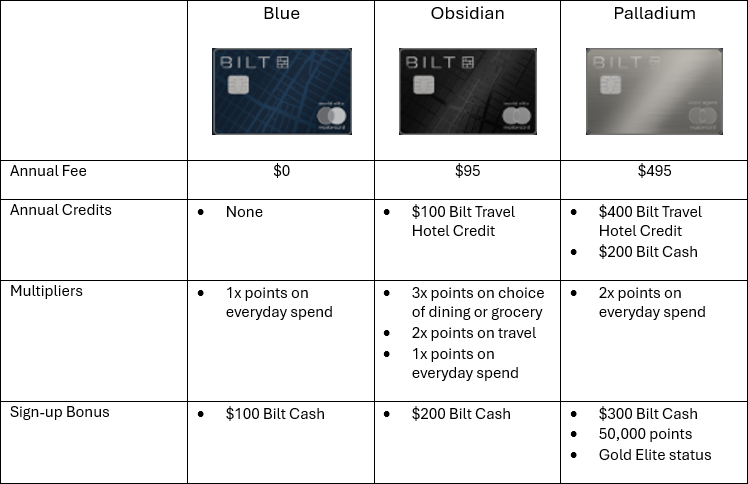

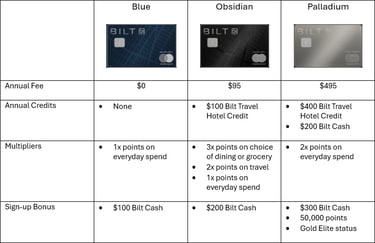

Card Offering:

The three card options offered by Bilt are the Blue, the Obsidian, and the Palladium. I outline the benefits of each in the table below. As a reminder, the rent options outlined above apply to all three options equally. There are no differences between the three cards in terms of rent. The differences are in the annual fees, points multipliers for non-rent purchases, credits and sign-up bonuses.

Max’s Takes:

Max’s Take on Rewards Membership:

When linking any account to your Bilt Rewards Membership, you provide Bilt visibility to your entire spending pattern with that account. Bilt uses that information for targeted marketing and to help shape their offer. If you are comfortable with that, link away.

The list of partner restaurants can be a bit sparse, depending on your location. Get to know it before counting this benefit in your analysis.

Max’s Take on Rent Payment Options:

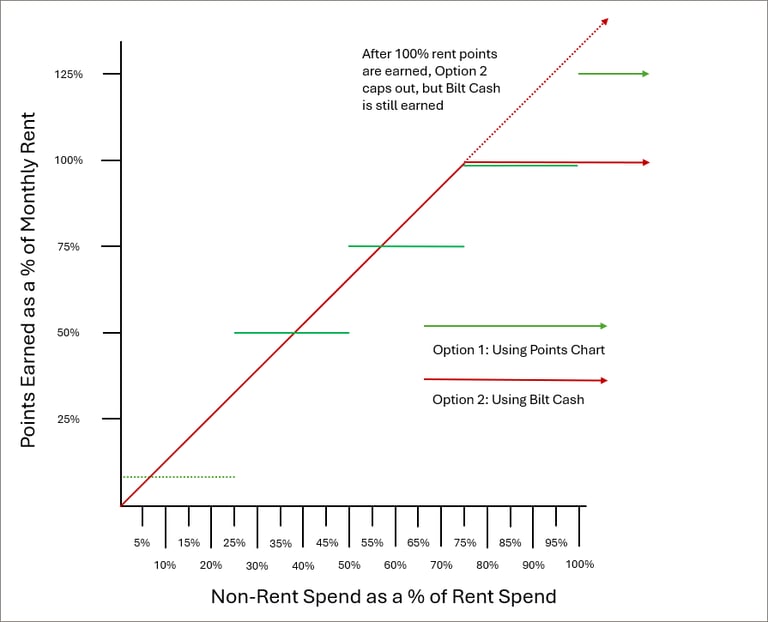

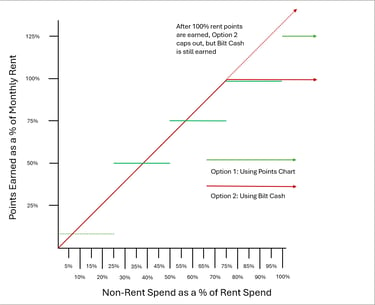

This is where things get really complicated. Which is the better option? It depends on how much your non-rent spend is in relation to your rent spend. The graph below compares the two options, irrespective of how much your rent bill is each month.

The horizontal axis shows non-rent spend as a % of rent spend, so for example, if your rent is $2,000 and you use your Bilt card for $1,000 on everyday purchases, your non-rent spend is 50% of your rent spend. The vertical axis shows points earned as a % of rent. So, if you are paying the same $2,000 in 100% points earned means 1,000 points.

The green lines reflect Option 1 - the chart. Note how they are tiered like a stairway. They reflect the thresholds established by the chart. If your non-rent spend is 25% of your rent spend, you earn 50% of your rent spend in points. If your non-rent spend is 35% of your rent spend, you still earn 50% of your rent spend in points, all of the way up to 50% of your non-rent spend, at which point you jump to earning 75% of your rent spend in points. The dashed green line reflects the base award of 250 points regardless of non-rent spend, which you don't receive with Option 2.

The red line reflects Option 2 - Bilt cash. In this option, Bilt cash is converted to unlock points for rent spend. The red arrow reflects a steady increase in rent points as the non-rent to rent spend ratio increases. It continues this way until the points reach 100% of rent spend, at which point it is capped. However, after that cap you will continue to earn Bilt cash as your non-rent spend increases. That Bilt cash can be used to free up rent points in future months, or it can be redeemed dollar-for-dollar for monthly credits across the Bilt ecosystem, or for exclusive benefits like higher transfer bonuses and special access to experiences.

Drawing a vertical line up from your projected non-rent to rent spend ratio shows which option is better for you. In general, Option 1 (the chart) is a better option when your non-rent spend is much lower than your rent spend. As your non-rent spend increases in relation to your rent spend, Option 2 (Bilt cash) becomes the better option.

For free guidance on which option is better for you, contact us at email@maxyourplastic.com. We can walk you through the analysis and get you to the right solution.

Some good news is that you are not locked in once you have selected an option. You can change any time, and the change will take effect the following month.

Max’s Take on Blue:

A no-fee card is a good way to get into the points-for-rent game. The Bilt Cash bonus can be converted into points through rent payments, and has a value of 3,333 points. The Blue card also has some valuable additional benefits such as no foreign transaction fees, cell phone protection (this is legit, I have used it), purchase assurance, and rental car coverage.

Max’s Take on Obsidian:

Bilt advertises this card as targeted for “dining or grocery maximizers”. Once you choose your category, you’ll earn a minimum 3x points there. If you choose the dining category, you can earn up to 6x points at partner restaurants. The 2x travel points apply automatically any time you use the card to pay for flights, hotels, resorts, and car rentals.

The hotel credits are offered in two halves; one from January through June, and one from July through December. They are applied based on the date of payment. A minimum 2-night stay is required. To earn the credits, you must book through the Bilt Travel Portal. Price shopping is advised when doing this, as prices on the portal might be elevated, thus wiping out your entire $50 credit.

The Bilt Cash bonus can be converted into points through rent payments, and has a value of 6,667 points. In addition to the benefits provided by the Blue card, the Obsidian also provides trip cancellation and interruption, trip delay insurance, and extended warranty.

Obsidian’s benefits are strikingly similar to those of the Chase Sapphire Preferred, though it doesn’t have the strong eco-system of cards like Chase does to best maximize points. If advantage can be taken of the rent benefit, a strong case can be made that Obsidian is the better card.

Max’s Take on Palladium:

Bilt advertises the Palladium Card as their “most rewarding premium card”, though to point out the obvious, it is their only premium card.

The hotel credits are meaty enough to catch my attention, as it can reduce less expensive hotels down to almost nothing, even with the required 2-night stay.

Priority Pass, advertised as a $469/year value, is a swing and a miss. It seems rare these days that someone can walk right into a Priority Pass lounge with their membership. The lounges are frequently full, prompting lines, waitlists, or even flat out rejection. The first category of customers that gets denied entry?...the cardholders. Adding all of the Palladium users as members exacerbates the lounge overcrowding issues and further devalues the perk. I no longer see this as a significant benefit, even for the most frequent travelers.

The annual Bilt cash bonus of $200 (6,667 Bilt points) and 2x points on everyday spend are strikingly similar to the Capital One Venture X structure (2x points and 10,000 annual points bonus), but aside from the benefit of unlocking points for rent, the Venture X is superior to this card in every way, and it carries a lower annual fee.

The $300 Bilt Cash and 50,000 points sign-up bonus more than offset the first two years of annual fees, so they give plenty of opportunity to see if the Palladium is the right card for you. Gold Elite status results in some interesting rent day deals with transfer partners, reaching transfer value as high as 1.5:1.

In addition to the benefits provided by the Obsidian card, Palladium also provides insurance for baggage delay and lost or damaged luggage, and price drop protection.

Max’s Overall Take:

Bilt remains perhaps the most innovative credit card available, and has quickly developed the most robust travel partner collection of any card issuer. The ability to generate points through rent, and now mortgage payments, is a game changer. The prior structure of earning 1 point per dollar of rent in exchange for using the card 5 times for everyday purchases was not profitable for Bilt and is long gone. Now, to unlock points for rent, the card must be used for significant purchases.

The key to getting the most value of these cards is through a strong spending to rent ratio. If rent is low and spending is high, the value will be maxed. If rent is high and spending is low, most, if not all, of the rent points will remain locked away. In such circumstances, the card user is faced with a decision to use the card more for everyday spend or leave those rent points locked up. That additional spend may come at the expense of not using other cards whose reward structure for those purchases is greater. Even so, if you can take advantage of the rent benefit, it makes sense to have one of these cards in your wallet.

If you'd like any specific guidance on whether a Bilt card is right for you, and if so, which one, please contact me at email@maxyourplastic.com. My services are free of charge and there are no obligations.

If you'd like to apply for a Bilt card, please use the link below. I'll get a referral fee, paid by Bilt, and it will cost you nothing.

If there are any other topics related to extracting maximum value from your credit cards you would like to learn more about, please let me know!

Max Your Plastic

Let your credit cards take you to new places.

Contact us

email@maxyourplastic.com

© 2025. All rights reserved.