Bilt Mastercard - How it Works

Max Your Plastic Report

Craig Turck

3/5/20254 min read

Introduction:

The Bilt Mastercard is innovative, but there is a lot of misunderstanding about how it works. This article addresses three commonly asked questions about the card, and explains the underlying process that makes it possible:

“My landlord doesn’t accept credit cards, whether they charge transaction fees or not. Why would they accept the Bilt card?”

“If I link my other credit cards to the Bilt Mastercard, do I really cash in on the points both cards have to offer?”

“Will using the Bilt card for rent affect my credit score?” and, if so, “How can I prevent this?”

“My landlord doesn’t accept credit cards, whether they charge transaction fees or not. Why would they accept the Bilt card?”

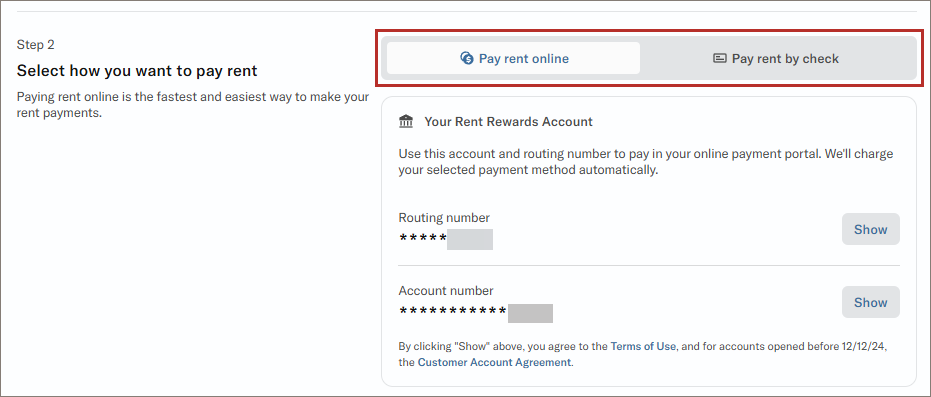

Quite simply, your landlord will accept the Bilt card because they are not being paid by credit card. Confusing? Let’s break it down.

When you set up your card, you’ll provide your landlord’s information and establish how you want them to be paid. You have the option of paying online via ACH, or paying by check. That is all the landlord sees. They don’t know a credit card is even involved.

You make the payment with the appropriate designation in the Bilt app, and the charge appears on your credit card statement (unless you have set up BiltProtect. See below.) which you pay monthly, just like any other card.

“If I link my other credit cards to the Bilt Mastercard, do I really cash in on the points both cards have to offer?”

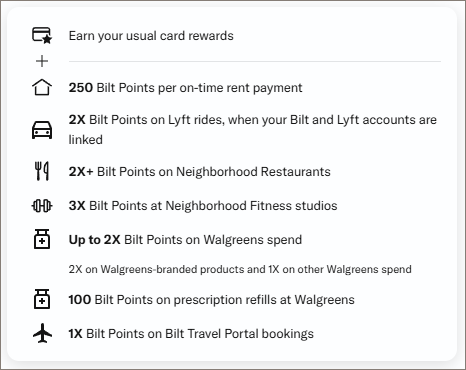

Yes and no. The points do stack, but not completely. You will receive all of the benefits you normally receive from your linked card when you use it, but the Bilt points are reduced from their standalone value. The image below reflects the Bilt benefits associated with a linked card:

We can see some key changes from the standalone Bilt offer:

The 3x points at restaurants is no longer there

Since you would be using another credit card, the 3x Lyft points for using the Bilt card to pay are gone

There are no longer points for booking directly with airlines, hotels and rental car agencies

Most importantly, if you use a linked card to pay for rent, you are capped at 250 Bilt points

As an example, Amex Gold gives 4x points for dining at restaurants. If that card was linked to the Bilt card and you dined at a restaurant offering 3x partner points, you would receive 7x points for dining (4x with Amex and 3x with Bilt). If you used your Bilt card at the same partner restaurant, you would receive 3x points + 3x partner points, or 6 Bilt points in total. The increase is only 1 point.

Similarly, if you link a Chase Sapphire Reserve card to the Bilt card, you would receive 7x points on Lyft rides (5x with Chase and 2x with Bilt) instead of 10x (5x with Chase and 5x with Bilt). 7x points is better than the 5x points you would receive with Bilt alone, but it is not a complete stack.

In exchange for this you are providing Bilt with visibility to the transactions on the linked card(s). The contract terms and conditions state that this is to identify qualifying purchases, determine eligibility for the program, operate and analyze the effectiveness of the payment card linking. That being said, in the same paragraph the phrase “Notwithstanding anything to the contrary…” is used TWICE, both of which indicate there might be contradictory language elsewhere in the terms and conditions. Proceed with caution.

“Will using the Bilt card for rent affect my credit score?” and, if so, “How can I prevent this?”

It can, though it can be offset, and even improved, by activating BiltProtect.

Your credit score is based on multiple factors, one of which is amount owed vs. available credit. If this ratio is high (meaning you are using a lot of your available credit), this may indicate you are overextended, and banks can interpret this to mean you are at a higher risk of defaulting.

If your Bilt credit limit is $7,500, and your monthly rent is $4,000, then you are already using a lot of your available credit. Using the card for additional charges pushes it even further.

BiltProtect lets you pay rent without using your credit limit, by pulling the full rent payment directly from a linked bank account. This means that when you pay rent, the charge doesn’t hit your card, leaving the entire $7,500 credit limit available, and keeping your credit use very low. You still receive the Bilt points for paying rent.

A word of caution using BiltProtect. You are responsible for ensuring there are sufficient funds in your linked bank account to cover each rent payment. Failure to do so can result in incurring fees or penalties from your landlord, and/or fees and interest from Bilt.

Summary

The Bilt card is innovative and flexible. These attributes have led to misconceptions about how the card works. I hope this answers any questions you may have. If you do have additional questions, reach out to me on my facebook page or email me and I’ll do my best to respond to you promptly.