HOW CREDIT CARD COMPANIES MAKE MONEY, AND HOW YOU CAN TAKE ADVANTAGE OF IT

ANALYSIS

Craig Turck

8/25/20257 min read

Introduction:

Banks are literally hauling in billions of dollars each year through the authorization and use of credit cards. To attract customers, they are pouring millions back into enhanced card benefits and welcome offers. This, they know, will enhance loyalty and increase their customer base, paving the way toward greater profits.

This landscape creates unique opportunities for us, as consumers, to share in some of the banks’ profits. If managed responsibly, we can take our share of the millions the banks have put on the table to live a better life!

This article covers:

The Parties Involved

How Banks Make Money from Credit Cards

The Real Cash Cow

How Banks Increase Their Credit Card Income

How You Can Claim Your Share and Enjoy the Benefits

The Parties Involved

First, let’s define the parties involved in credit card use to help eliminate confusion as we explain where the money is flowing:

Cardholder – Those using credit cards to buy goods and services (AKA, us)

Card Issuer –The banks who offer the credit cards, and through whom we receive card benefits. Examples of card issuers are Chase, Citibank, Capital One, Wells Fargo, American Express*, etc.

Merchant – The entity from which the cardholder is buying goods or services.

Credit Card Network Companies – The companies providing authorization, clearing, settlement, network access, and other services that enable transactions. Examples of network companies are Visa, MasterCard, and American Express*

Travel/Award Partner – companies from whom card issuers purchase service credits which, in turn, are offered to cardholders in the form of awards and bonuses.

*American Express is unique as they often act as both the card issuer and the card network company.

How Banks Make Money through Credit Cards:

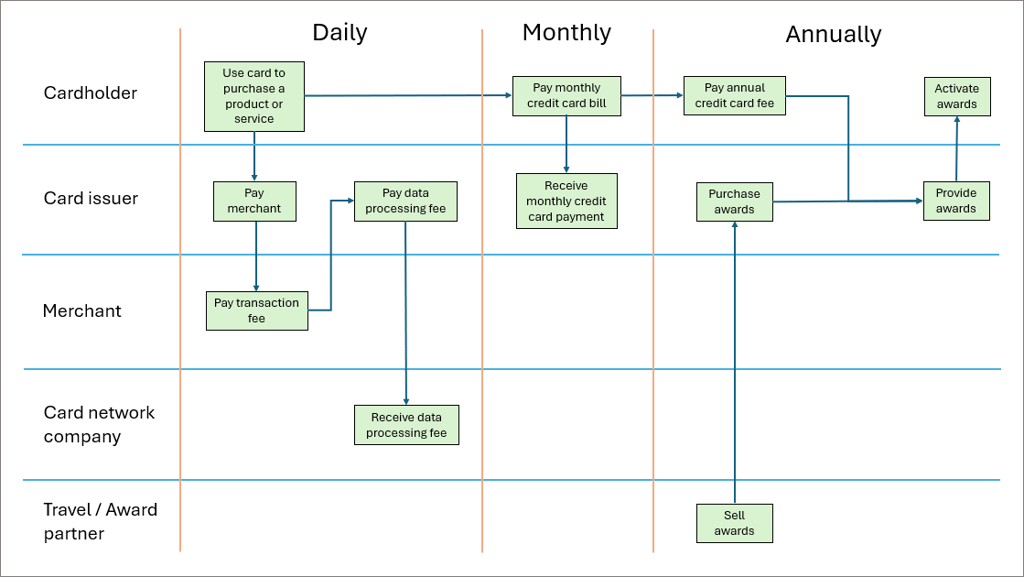

Let’s start with the basics. We go to the store, find something we like or need, then head to the cashier and pull out our credit card to pay. We tap, swipe, or insert, and after a beep sounds, we leave with our merchandise. But how does this work?, and where is money being made? The text and flow chart below should help to make this clear.

A large portion of the money comes from Transaction Fees. These are fees that the card issuer charges the merchant every time one of us taps, swipes, or inserts a card. This fee is usually between 1.5% and 3% of the total purchase. Sometimes the merchant adds this fee to the price, thus passing the burden onto the cardholder, but usually they absorb it. Using 2020 data, Transaction Fees accounted for almost 30% of the credit card industry income.

At the end of the month, the cardholder is responsible for paying the debt accumulated to the card issuer. If the cardholder pays in full, the issuer does not make any additional money. We’ll come back to this.

There are a wide variety of credit cards available to consumers. Some have no annual fees, and some carry significant annual fees, even over $500. The cards with annual fees, of course, bring with them awards, credits and other benefits which entice the cardholder to shell out this cash annually. In many cases, they are worth the cardholder’s investment. This is case by case dependent.

The card issuers purchase such benefits from Travel / Award Partners, and pass these directly to cardholders.

Again using 2020 data, annual fees accounted for about 7.5% of industry income.

If you are interested in a credit card and want to find out which one is right for you, contact us as email.maxyourplasic.com for free guidance.

The Real Cash Cow

So, transaction fees and annual fees accounted for almost 40% of industry income in 2020. Where did the rest of it come from?

Interest and Penalties accounted for HALF of industry income in 2020! Interest alone accounted for 43% of industry income! We incur penalties when we don’t pay any portion of our credit card bill, and these account for 7% of industry income! These numbers are hard to believe, but they are accurate.

Card issuers charge interest rates which range from roughly 15% to roughly 35%. There is no investment any of us can make that will deliver that type of interest income sustainably over time, so to pay such an interest rate is downright foolish.

Yet many of us do.

Why? For many of us, it is because credit cards enable us to spend money we don’t have. If we’re living paycheck to paycheck, a credit card might enable us to purchase for a need with the hopes we can save up that money by the time the bill comes due. It could also entice us to buy something we don’t need, even if we know we don’t have the money to cover it.

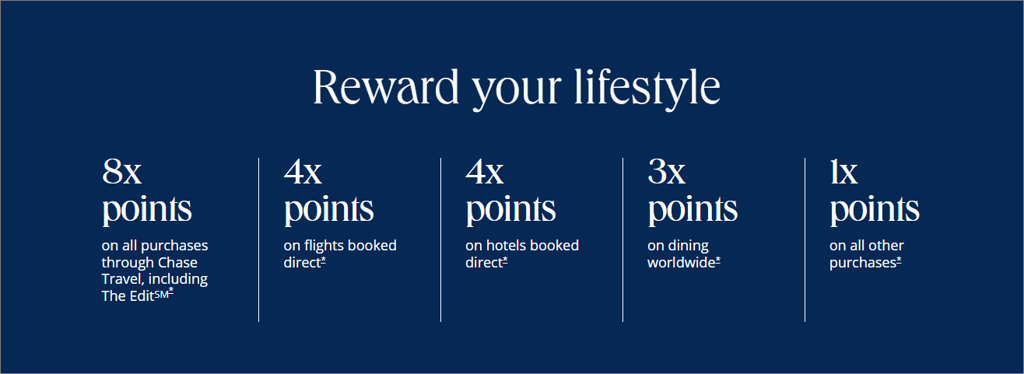

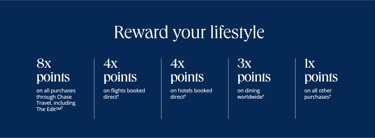

Cardholders are also retained through ongoing benefits, particularly benefits that renew annually or periodically. Airline credits, hotel credits, points multipliers and annual bonus points are all examples of these. Below is an example of points multipliers offered through the Chase Sapphire Reserve card.

Cardholders are enticed to spend money they normally wouldn't through credits offered by the card issuers. An example of this might be a credit at a luxury hotel normally outside of the cardholder budget. The credit covers only a portion of the cost of the overall stay, but it may be enough to make the cardholder feel the splurge is worthwhile.

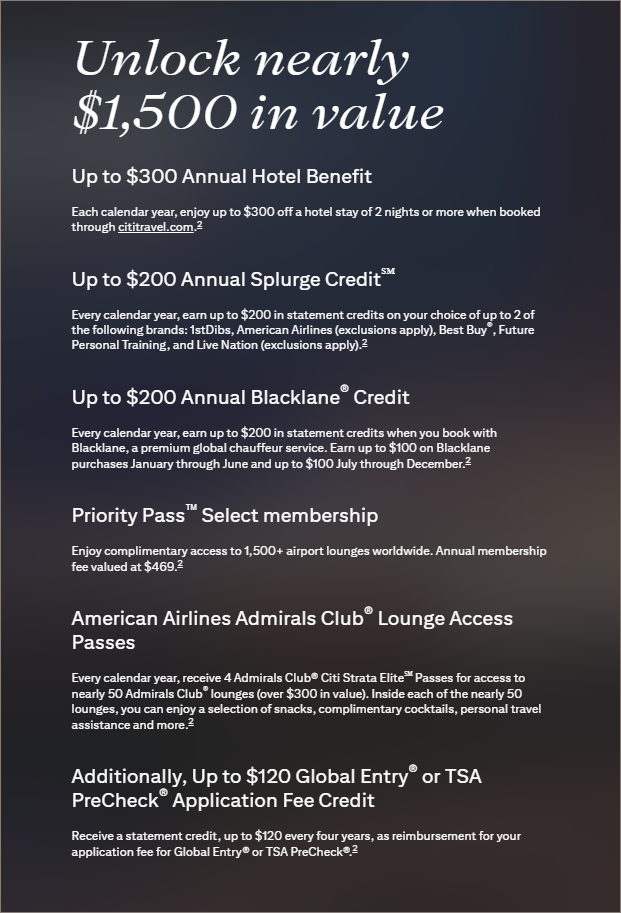

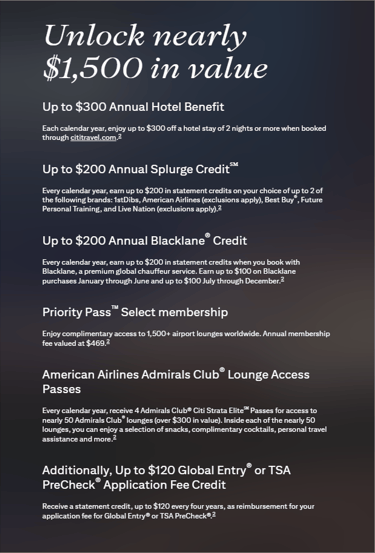

Check out these enticing credits offered with the Citi Strata Elite card.

While these enticements are focused on increasing the bottom line for the banks, if used wisely they can be of great value to the cardholders.

How You Can Claim Your Share and Enjoy the Benefits:

So, the banks are hauling in billions and want to haul in more. To do this, they provide consumers with incentives to obtain, retain, and use their cards. The money, so to speak, is on the table. With disciplined use of credit cards, you can pull money off of the table without incurring any cost. Here are four keys to making this happen:

1. Pay your credit card bills in full every month.

Stay away from the insane interest rates credit cards charge! Zero % introductory annual percentage rates and pay over time offers can be very attractive, but they can also put you in a hole that is hard to dig out of.

2. Don’t change your spending habits

Credit cards do not make things affordable…your income still has to do that. Don’t let the convenience of a credit card, or incentives provided by the issuer, lure you into spending money you normally wouldn’t. When considering a credit card with an annual fee, assess whether the credits offered by the card offset the fee based on your current spending habits. If you have to change your spending habits to take advantage of a credit, you're spending money to save money, and that credit is not really saving you money.

3. Enjoy the welcome bonuses as you curate your credit card portfolio to best match your spending habits.

Card issuers offer points, miles, and cash back simply for opening an account and meeting minimum spending criteria. Depending on how points are valued, these offers can be worth over $4,000…just for opening an account! The card issuers offer this to expand their cardholder base, and because they know that the aggregated money they make in transaction fees, interest and penalties will more than offset this cost. If you use your cards wisely, that money is there for the taking.

4. Get the credit cards that maximize your returns

Why settle for 2% cash back when you can get 5%? Why settle for 1 point per dollar spent when you can get 10 points? Does a credit card offer free credits in areas you spend money today? Matching the right credit cards to your spending habits will unlock these credits, help you get more cash back or earn points more quickly, so you can take that dream vacation you’ve been waiting for! Contact us at email@maxyourplastic to set up a free consultation session on maximizing the returns on your credit card use.

Please let me know your thoughts on this article or let me know if there are any other credit card or travel topics you’d like me to write about on Max Your Plastic.

The credit card network companies also charge for each transaction, as they are performing the data processing for each. These are paid by the card issuer, thus the network companies and issuers are sharing in the 1.5% to 3% transaction fee. The card issuers also pay the network companies for the use of their name in marketing.

Credit card interest can accumulate quickly, and if we want credit cards to work for us, we need to do whatever we can to avoid it. See my page Rules of the Game for more on credit card interest, including an example of how this interest can escalate out of control.

We incur penalties when we don’t pay any portion of our credit card bill, and these penalties still account for 7% of industry income!

How Banks Increase their Credit Card Income

Even with their screening process, banks can’t predict our individual spending and payment behavior. However, when their cardholders number in the millions, spending and payment behavior predictability becomes very precise. Therefore, the best way for banks to increase their income is to drive an increase in credit card spend.

There are three primary ways banks can drive this increase: generate new cardholders, retain existing cardholders, and entice both groups to spend more with their cards.

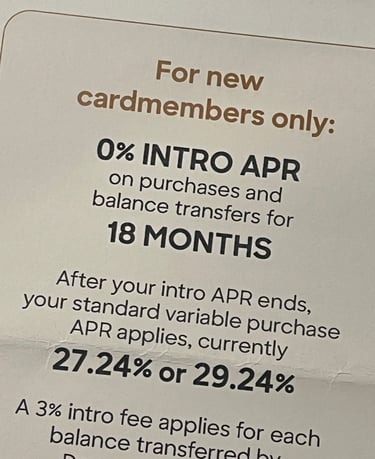

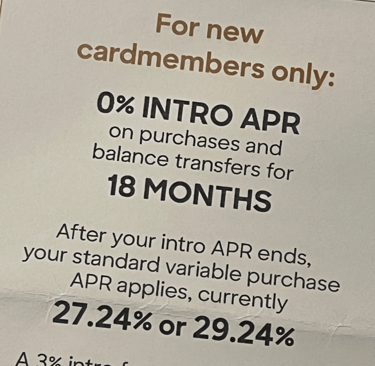

Attractive introductory offers and ongoing benefits attract new cardholders. Sign up bonuses, cash back, and low or zero APR are examples of introductory offers. Below is an example of an introductory offer.

Max Your Plastic

Let your credit cards take you to new places.

Contact us

email@maxyourplastic.com

© 2025. All rights reserved.