HOW YOUR CREDIT SCORE IS CALCULATED...

...and How Your Use of Credit Cards Impacts That Score

ANALYSIS

Max Plastic

12/15/20257 min read

Introduction:

Most of us know that a higher credit score is good for us, but do we know the impact the score has on our financial well being? Our credit scores can affect:

our ability to get a loan to pay for a new car or home

the interest rate on a new loan

whether or not we are approved for a new credit card

the amount of credit that may be extended to us

But how do we increase our credit score? If we are able to earn an exceptional score, how do we keep it there? How does use of credit cards affect our score?

In this article, we’ll answer all of these questions and more by looking at how the credit score is determined by component, and how our actions affect each of those components. Credit score calculations are quite complex, so to keep this article length reasonable, several simplifications have been made.

This article covers:

What is a Credit Score?

Credit Score Tiers

Components of a Credit Score

Payment History

Credit Utilization

Length of Credit History

New Credit

Credit Mix

How to Check Your Credit Score

Summary

What is a Credit Score?

A credit score is an independent assessment of the likelihood of a borrower to repay loans provided to them. There are two primary scoring methods, FICO and VantageScore, and several different versions of each. While very similar in general, each version is slightly different and is an attempt to be more accurate in assessing credit worthiness for a particular situation. When applying for credit, it is important to know which scoring method is being used so you can assess where you stand, and what you can do to best improve that score. It is worth noting that FICO scores are used by 90% of top lenders, and this is the score we will be analyzing in this article.

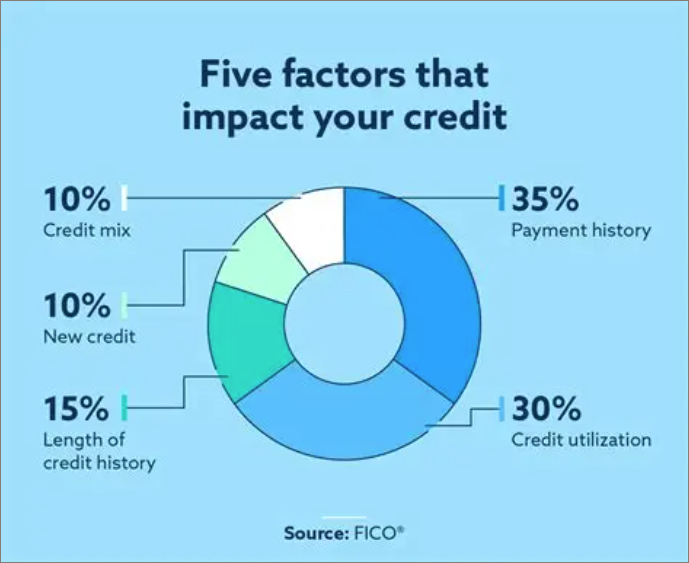

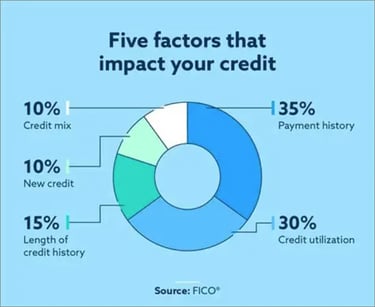

There are five key components to a credit score. They are Payment History, Amount of Debt, Length of Credit History, New Credit, and Credit Mix. We will look at each of these in more detail.

Combined, these scores total between a range of 300 and 850.

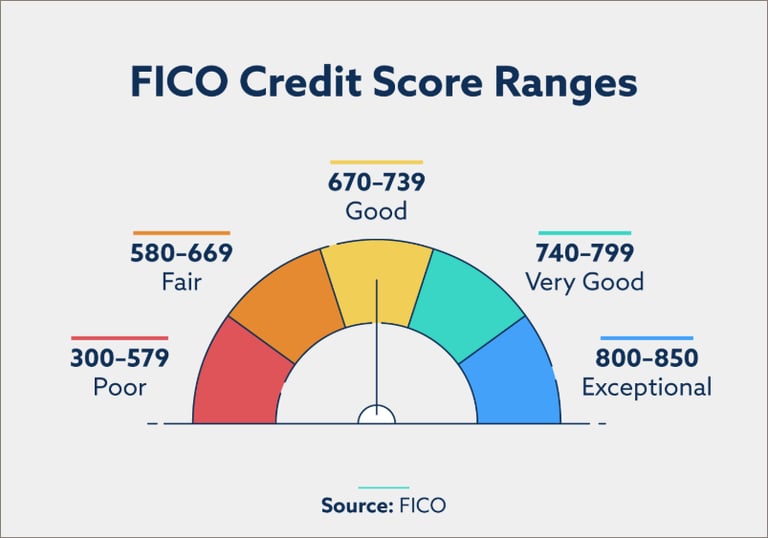

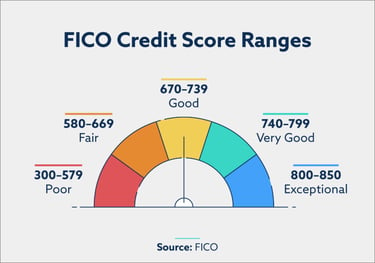

Credit Score Tiers:

There are tiers within this range which determine an individual’s credit worthiness, ranging from poor to exceptional, as shown in the diagram below:

The tier in which your credit score falls determines whether you might qualify for credit, and if you do, how much credit you might be extended and the interest rate charged for repayment.

For example, a borrower might be flat out rejected for even an introductory credit card if their score falls in the poor range. Applicants for premium cards, like the Amex Platinum, might only be approved if their credit score is exceptional. In addition, the credit limit established for a card applicant with an exceptional score might be $30,000 vs. $5,000 for an applicant with a Good score.

Interest rates on mortgage and auto loans could vary significantly based on credit score. With current rates, the difference between a credit score of 675 and 775 likely results in a mortgage interest rate difference of more than ½% on a $500,000, 30 year fixed loan. That doesn’t look like much, until one sees that translates to about $50,000 more interest paid over the life of the loan!

For auto loans, the interest rate for someone with poor credit can be more than twice that of someone with very good credit, again more than doubling the amount of interest paid over the life of the loan. For a $25,000 loan, that can translate to $8,000 more in total payments!

Failing to increase and maintain a higher credit score can be very expensive, indeed!

Payment History (35%)

This component carries more weight than any other in determining your credit score. Have you made any payments 30 days late? 60 days late? Have you defaulted on a loan? Each of these impact this factor in increasing order. One 30-day late payment can cause a drop of 60 to 110 points, depending on your credit history. The amount of time that has passed since your last late payment also impacts this factor; the more recent the late or missed payment, the greater the impact. A missed payment will remain on your report for seven years.

To maximize this component of your credit score:

Establish a history of on-time payments on all loans, including credit cards. This takes time to build, and any missed payment can set you back significantly.

Credit Utilization (30%)

Credit utilization is a ratio determined by the sum of the balances on revolving accounts, like credit cards, divided by the sum of the credit limits. The lower this ratio, the better. A ratio below 10% is considered excellent. A high ratio, above 30%, could indicate to creditors that you are leveraged too highly and present a risk. As an example, if an individual has three credit cards, each with a $10,000 credit limit, no other revolving debt accounts, and currently owes $5,000, their credit utilization ratio is 17%. Creditors are comfortable with this.

To maximize this component of your credit score:

Request credit limit increases from your card issuers. Card issuers are open to this and there is a good possibility of success.

Pay off credit cards more frequently. This keeps outstanding balances down, thus lowering your utilization ratio. This has particular impact if there was a recent, significant charge on one of your cards.

Length of Credit History (15%)

This component factors in the average age of accounts, and the age of the oldest account. A strategy of rotating through credit cards to max out on welcome offers will have a negative impact on this element. Finding the right cards for yourself and keeping accounts open for a long duration help in this area.

To maximize this component of your credit score:

Keep your oldest credit card, regardless of whether it is valuable to you any more, particularly if there is no annual fee associated with it. It serves as excellent ballast as you curate the remainder of your credit card portfolio to maximize value.

New Credit (10%)

Only 10%. This is likely because everybody is likely to have some changes in the credit cards they use over time, as well as multiple auto loans and mortgages in their lifetimes. This component is impacted by the age of your most recently opened account and the number of recent credit inquiries. This component is a significant fear in most clients I serve, and it is mostly unfounded.

The typical drop in credit score resulting from an inquiry is 2 to 5 points. Even if rate shopping for a mortgage or auto loan, multiple inquiries within a short timeframe may be treated as a single inquiry, thus minimizing the impact. Also, if the inquiry results in a new credit card account being opened, the Credit Utilization ratio improves, thus offsetting the impact of the credit inquiry in a short period of time.

To maximize this component of your credit score:

Take advantage of pre-approval offers from credit card issuers. This allows them to give a preview of whether you will be approved for a particular card. Pre-approvals use “soft” credit inquiries, which do not impact your credit score. They also reduce “hard” credit inquiries for cards which might have been denied you.

Limit credit card churn. Research which cards bring you the most benefit and create a plan before applying for cards with attractive welcome offers. Contact us at email@maxyourplastic.com for free credit card consultation. For an excellent score in this element, the most recent account should have been opened about 3 years ago. Most people with excellent credit scores have not had an inquiry within the past 12 months.

Credit Mix (10%)

This component looks at the total number of credit accounts being used or reported, including credit cards, retail accounts, installment loans and mortgage loans. Student loans, auto loans, and personal loans all count toward this. A healthy credit mix demonstrates to lenders that you reliably manage a variety of credit accounts. For most people with established credit, this component is already maximized. Opportunities for improvement are generally applicable to new borrowers looking to establish credit.

To maximize this component of your credit score:

Become an Authorized User on someone else’s account. This enables you to begin building credit without needing to be approved for your own account.

Open a secured credit card account. These accounts require a security deposit up front to use them, so you are at least sharing in the credit risk.

How to check your credit score:

Checking your credit score today is easy. Many credit cards issuers offer this service for free when you open an account with them. You can also set up a free account with experian at experian.com

Summary

The most important consideration in taking on any credit is your ability to pay off that debt. Failure to do so will damage your credit score in a way that takes years to repair, and lenders won’t want anything to do with you. If you can’t pay off your credit card balances in full each month, the interest rate will cost you dearly. For more information on credit card interest, check out my article “Rules of the Game” on my website.

There are five components to a credit score, each with varying weight. Your credit score is available to you, by component, along with suggestions on how to maximize each.

A healthy credit score is important. It gives confidence for lenders to make their money available to you. A healthy score not only makes it easier for you to get credit, but also gets you that credit at lower interest rates, thus saving you money.

Please let me know your thoughts on this article or let me know if there are any other credit card or travel topics you’d like me to write about on Max Your Plastic.

Email me at email@maxyourplastic.com for a free credit card consultation.

The Components of a Credit Score:

So, how are credit scores calculated?, and how can we increase them? The image below shows each component of the score and its relative weight in determining the score. We’ll take a look at what each one means, and how our use of credit cards can affect each component.

Max Your Plastic

Let your credit cards take you to new places.

Contact us

email@maxyourplastic.com

© 2025. All rights reserved.