9 WAYS TO MAXIMIZE POINTS AND CASH BACK ON YOUR CREDIT CARDS YOU MAY NOT KNOW

BENEFITS UTILIZATION

Max Plastic

2/13/20267 min read

Introduction

Credit cards offer excellent benefits, from convenience and safety to cash back and points which can be used for discounted or even free travel.

The more of our yearly spend we place on our credit cards, the greater the benefits we receive.

Even savvy credit card users; however, may not be getting the maximum value from their credit cards because they don't realize some of the best ways to rack up points or cash back on their cards. Below are 9 terrific ways to build points or gain cash back through credit cards which might be news to you.

This article covers:

Taxes (Federal, State, and County)

Utilities

Auto

Home Improvement

Rent and Mortgage

Tuition and Childcare

Work Expenses

Venmo payments

Large Purchases

Max's Take

Taxes (Federal, State, and County)

There are several cards available which offer either 2% cash back or 2x points on all purchases. If a card receives 2% cash back, after the 1.75% fee it is bringing in a net 0.25% cash back. This may not seem like much, but it makes the transaction net positive. If your IRS debt is $10,000, 0.25% cash back is $25 in your pocket. It also brings the benefits of convenience (you can pay from home before filing), float (additional 30 days to make the payment), protection (nothing lost in the mail) and further building your credit score.

If a credit card earns points most, issuers offer cashing in the points at 1 cent per point at a minimum, so a card that earns 2x points brings at least the same value as a 2% cash back card. However, most points enthusiasts, like The Points Guy, value points at closer to 2 cents per point as they can be leveraged for deals with airlines and hotels. This would mean that a card earning 1x points would earn the same value as a 2% cash back card, and earning 2x points would clear a value of $225 with our tax bill of $10,000.

In addition, a large tax bill might put you in a position to open a new credit card where you could easily meet the minimum spend to earn a large sign-up bonus. Even a new card with no annual fee that earns 1x points would provide a bonus of anywhere from 30,000 – 100,000 points. That’s a value of $600 - $2,000!

Particularly large tax bills facilitate the opening of business credit cards, which usually require a greater spend minimum but offer an even larger sign-up bonus when that minimum is met. It can be seen in the images above that commercial and corporate cards are charged a higher fee by the IRS than personal cards. However, if paying through ACI Payments, a business card can be linked to PayPal, through which the payment can be made at 1.85%.

State tax agencies similarly charge fees for credit card payments, usually a bit higher, ranging between 2% and 2.5%. Even so, if the card offers 2x points or if it enables a sign-up bonus, paying state taxes with a credit card can be very beneficial.

If you have the ‘good fortune’ to live in a state where personal property taxes are charged, you’re accustomed to shelling out hundreds of dollars every year for the privilege of using your own car. As with state income taxes, the fees associated with paying that bill via credit card usually range between 2% and 2.5%, give or take. Again, in the right circumstances payment via credit card can be beneficial.

Utilities

Electricity, gas, water, sewage, trash, recycling. Most of us pay for all of these each month. Some of these may be charged through your local county or municipality, in which case similar fees to what you pay for taxes are charged.

However, electricity and gas are usually provided by independent companies, and therefore they may charge lower transaction fees, or no fees at all. Where I live, there is no fee to pay the gas bill via credit card, and the fee for the electric bill is a mere 0.9%. Using my card with 2x points for everything, this enables me to build roughly 10,000 points annually with minimal fee. 10,000 points is enough for a free, one-way domestic flight!

Auto

Home Improvement

Hiring a contractor for a large home improvement or maintenance project? Find out up front which bidders accept payment via credit card and take that into account when analyzing bids. Your credit card might be the deciding factor for awarding the work. Like your taxes, this can represent a significant expenditure and may present an excellent opportunity to open a new account with a good sign-up bonus, increasing the value of paying by card.

Rent and Mortgage

Yes! You can even use a credit card to pay your rent and/or mortgage. Even though your landlord/lender may charge a transaction fee, or may not accept credit cards, the Bilt credit card waives the transaction fee and makes the card transaction invisible to them. It even awards you points for these dollars spent. It’s not quite that simple, but given the upside it is worth investigating how these cards work. For more information, check out my article on the latest version of these credit cards here.

Tuition and Childcare

These are two additional potentially significant expenditures, which represent a significant potential for earning cash back or points. Granted, you’ll probably run into a 3% transaction fee for these expenditures, but as I’ve mentioned before, in the right circumstances that transaction fee might be worth it, particularly when opening a new card account.

Work Expenses

If you own your own business, this is a no-brainer. You probably have a business card account and have your employees use the same. If, however, you work for a smaller company who hasn’t set up something similar, this represents a great opportunity to earn free money. You incur business expenses, pay for them with your credit card, submit to your company for reimbursement, and cash in on the cash back or points provided by your credit card!

Venmo Payments

Large Purchases

Appliances, jewelry, electronics, you name it. Of course, this almost goes without saying, but expenditures like these present a terrific opportunity to open a new card account and make great progress toward, if not even meet, the spend requirements to qualify for the sign-up bonus.

Max’s Take

Credit card issuers offer incentives to open accounts with them and use their cards. They make profit on the cards through interest and penalty fees, transaction fees, annual fees in some cases, and other miscellaneous sources. To generate this revenue, they offer incentives to attract us to open accounts with them and to use their cards. The more card holders they have, the greater the income.

By using the cards responsibly and avoiding interest and penalties, the use of credit cards can be very beneficial to us. We can unlock lucrative sign-up bonuses for opening accounts, and earn cash back or points for using them on things we would need to buy regardless. If we need to spend $20,000 per year, why not earn at least 2% back on that and enjoy the $400 bonus? Or earn at least 40,000 points…enough for two domestic round-trip airfares?

The more spend we can place on our credit cards, spend we would incur whether we have credit cards or not, the greater the benefits we earn. The 9 opportunities listed above should help you to ensure you are maximizing your credit card spend, thus maxing your plastic!

Do you have any other opportunities for maxing your plastic you would like to share? Feel free to respond with your comments.

If you would like further guidance on how to maximize the value of your credit cards, please reach out to me at email@maxyourplastic.com to set up a free, no obligation consultation.

Ugh! Who likes paying Uncle Sam?!? Nobody! That being said, the use of credit cards can take the edge off.

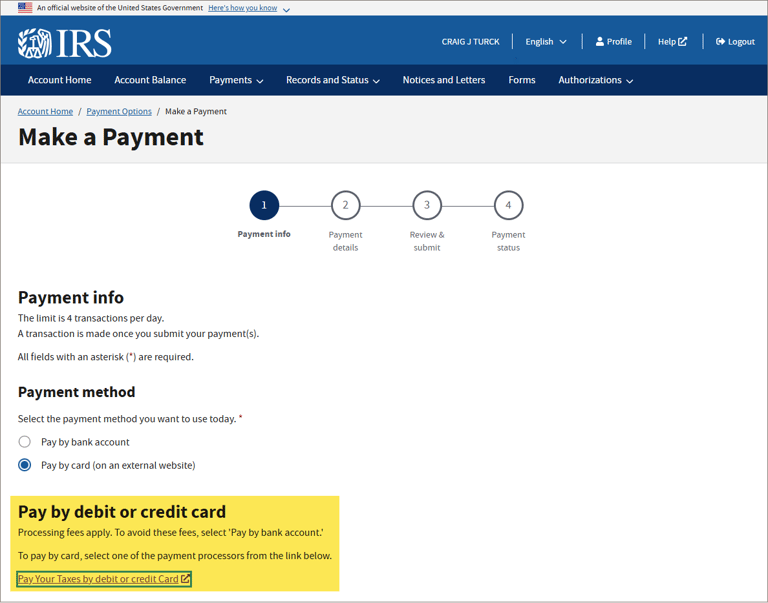

The IRS offers multiple means of payment, including credit cards. To make a payment via credit card, in the Make a Payment screen of the IRS website, select 'Pay by debit or credit card'. The IRS uses two payment processors, Pay 1040 and ACI Payments, each of which charge a fee for credit card use, 1.75% and 1.85% respectively. This may turn some of us off to the idea of paying with cards, but let’s dig into it a little more deeply.

Car dealerships don’t want you to know this. They may claim they do not accept credit cards because 1) they don’t want to pay the transaction fee (from the dealership perspective, allowing you to pay via credit card is like providing you a 3% discount), and 2) they would prefer the loan be financed through the auto manufacturer, bringing greater profit to the manufacturer. As we know, however, everything at an auto dealership is negotiable. It’s up to you to determine when the best time is to bring this up, whether it is up front, after negotiations are complete, or somewhere in between. One good time might be right after they surprise you with the “dealership fee” that was not mentioned in negotiations. It is not likely they will allow you to finance the entire purchase with your credit card, but $5,000 might be doable.

At the time of writing this article, Venmo allowed you to link two credit cards to your account, American Express and Bilt. Doing this means that, instead of Venmo charging your bank account, they charge your credit card, which generates points for you when you pay the card bill. To ensure this happens, be sure that you have transferred all monies in your Venmo account to your bank account so it will not draw from available funds in Venmo first. Link your credit card to Venmo. Then select your credit card as your funding choice for the payment.

Max Your Plastic

Let your credit cards take you to new places.

Contact us

email@maxyourplastic.com

© 2025. All rights reserved.